Now that we’ve established the importance of a term insurance plan, did you know that it offers you complete freedom of choice when it comes to premium payment options? That’s right. Nearly all term life insurance policies come with multiple different premium payment options. Continue reading to find out more about them. And to understand them better, let’s first quickly take a look at how term insurance actually works.

How Term Insurance works

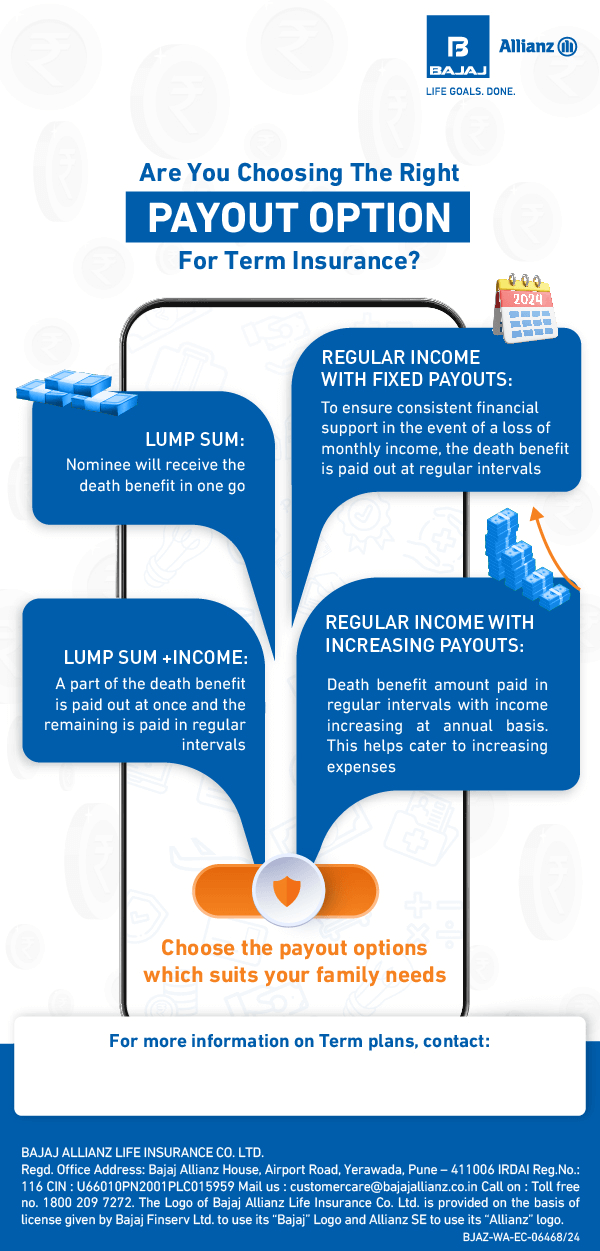

A term insurance policy is essentially a contract between an insurance service provider and an individual. According to the contract, the insurer agrees to provide the individual, known as the policyholder, with a life cover of a predetermined sum for a certain period of time. The life cover, also known as the death benefit sum assured, is paid out to the nominee in the event of the policyholder’s death. The death benefit can then be used by the nominees of the deceased to further their life goals. However, if the policyholder survives till the end of the policy tenure, they would not receive any sort of maturity benefits.

What is Term Insurance Premium?

Now, in exchange for receiving the life cover, the policyholder has to pay a certain sum of money periodically to the insurer. These payments that the policyholder makes are what are referred to as premiums. And when the premiums are paid to the insurer on account of having a term insurance policy, they’re known as term insurance premiums.

Types of Term Insurance Premium Payment Options in India

As you’ve already seen above, term insurance premium needs to be paid by the policyholder periodically. The frequency and type of premium payment depends on what the policyholder chooses at the time of purchase of the policy. Currently, there are as many as three different types of premium payment options in India. Here’s a brief overview of these options.

1. Regular Premium Payment

This is one of the most popular premium payment options that policyholders choose. Here, the policyholders are required to pay premiums regularly till the end of the policy tenure. For instance, if you take a term insurance policy for a tenure of 10 years, under the regular premium payment option, you would have to pay premiums regularly throughout the entire 10-year tenure.

With the regular premium payment option, most insurers allow you to customize the frequency of payments. You can choose to pay premiums on a monthly, quarterly, half-yearly, or annual basis. Again, for instance, if you choose the monthly premium payment option, under the regular premium payment option, you will have to pay premiums each month till the end of the policy tenure.

2. Limited Premium Payment

Limited premium payment is another option that you have as a policyholder. Unlike the first option, here, the duration of premium payment is lower than the policy tenure. This effectively means that you wouldn’t have to pay term life insurance premiums till the end of the policy tenure. Here’s an example that can help clear things out for you.

Assume that you wish to purchase a term life insurance plan with a tenure of around 10 years. Under the limited premium payment option, you wouldn’t have to pay premiums till the end of the tenure of 10 years. Instead, you would only have to pay for a limited period of time, say 5 years. Once you’re done paying the premiums for the first 5 years, you can relax during the remaining 5 years of the policy tenure - without having to pay any premium.

And similar to the previous option, you get to choose the frequency of premium payment as well under limited premium payment.

3. Single Premium Payment

As the name itself signifies, the single premium payment option requires you to make just one premium payment during the entire tenure of the policy. The policy will continue to be in force till the end of the tenure even without having to pay any more premiums. Here’s an example.

Say you wish to purchase a term insurance policy with a tenure of 20 years. Under the single premium payment option, you would only have to pay one premium at the time of purchase. Here, do note that since you’re only making a single payment for the entire duration of the policy, the premium under this option tends to be quite high.

An ISO 9001:2015

An ISO 9001:2015